Scrubbers seeing a faster pace of adoption

According to figures presented by DNV GL at Nor-Shipping 2019, more and more shipowners are switching to LNG and scrubbers. A total of 2,947 ships have already installed scrubbers, and this is expected to rise again in 2020 to a total of 3,502. The biggest surge was seen in 2018, as scrubber uptake quadrupled. However, current predictions indicate that scrubber adoption has peaked for the time being and will remain largely unchanged until 2023.

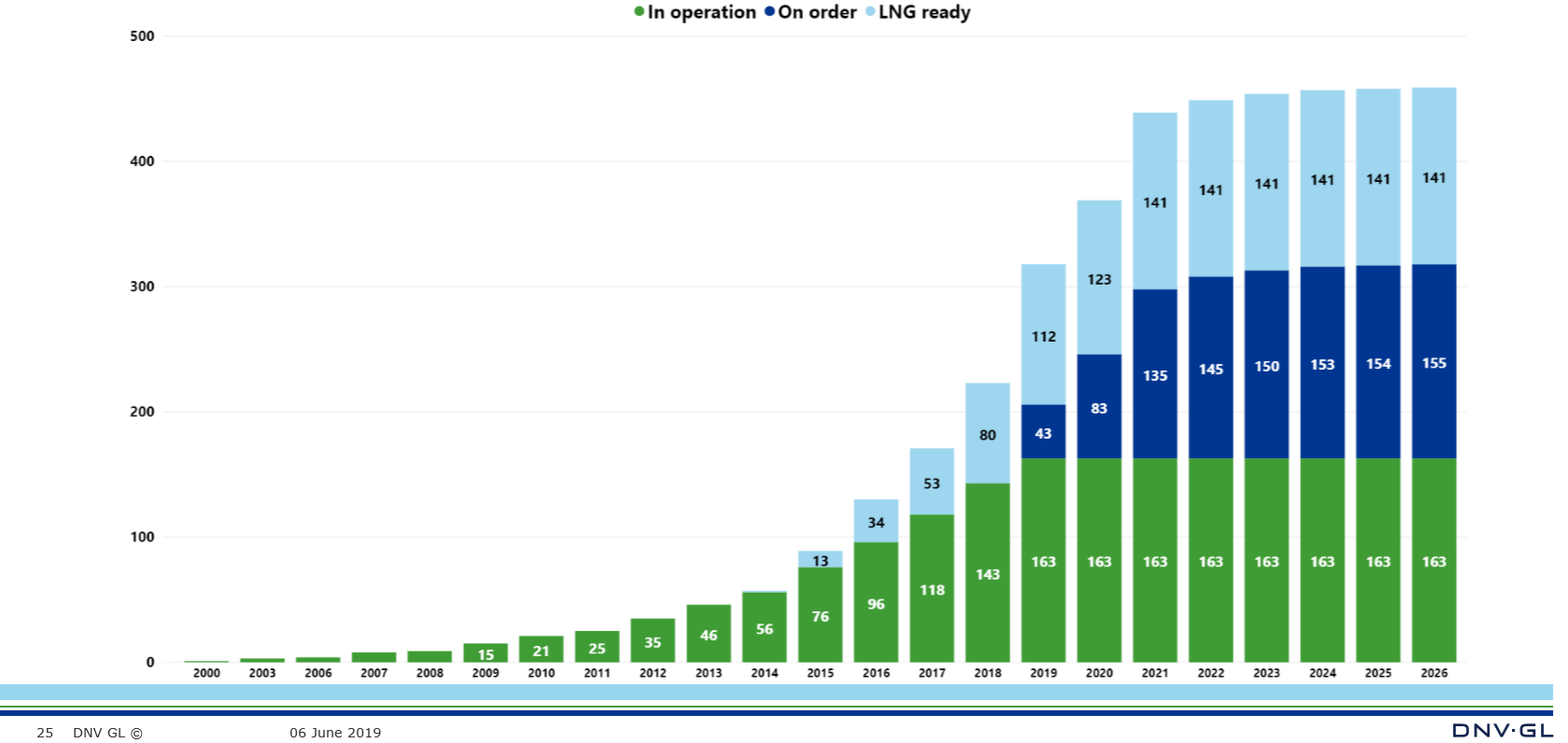

In terms of adoption, LNG lags behind at present. Just 163 LNG ships are in operation, while a further 112 ships are classed as LNG ready. DNV GL’s figures indicate that this number will stay steady for years to come, but orders will rise.

{kind=link}

LNG-powered vessels: the long game?

While LNG has had a comparatively slow start, the long-term outlook is brighter. In its Maritime Forecast to 2050, DNV GL predicts that by 2050 as much as 23% of the world’s fleet will be made up of LNG-powered vessels. This is based on the assumption that LNG bunkering infrastructure will be developed significantly in coming years. As converting a vessel from oil-power to LNG is a complicated process, the majority of growth in LNG as a fuel will be driven by newbuilds. Conversions are possible though. In August 2019, Hapag-Lloyd announced plans to convert one of its container ships to a dual-fuel LNG system in mid-2020.

In addition, many shipowners are taking a “wait-and-see” approach with LNG. While the alternative fuel has now been technically proven, there are still concerns about bunkering infrastructure and availability. Infrastructure development is underway in many regions, including North America, Asia, and many European coastal ports. If this development continues, demand for LNG-fueled vessels will begin to increase at a faster rate. Some industry sources believe that we have already seen the end of the “chicken and egg situation”, where bunker suppliers were waiting for the market and vice versa.

The trouble with scrubbers

Scrubbers allow vessels to continue to burn conventional high-sulfur fuel oils and still comply with the sulfur limit. This promise of “business as usual” is very attractive for shipowners who may have concerns about the price and availability of alternative fuels. While the installation of the system can be complex and cost millions of dollars, no changes need to be made to the engine or fuel treatment plant. This helps explain the comparatively quick rise in scrubber adoption compared with LNG.

However, recent discussions could cast doubt on the long-term viability of exhaust gas cleaning systems. Open-loop scrubbers in particular are coming under greater scrutiny for the washwater they discharge. Critics state that this is simply trading one type of pollution for another, or taking sulfur out of their air and putting it in the ocean. This has led to bans on open-loop scrubbers in China, Singapore, and Fujairah in the United Arab Emirates, as well as individual ports in Finland, Lithuania, Ireland, and Russia. On the other hand, more than 20 ports have sent no-objection letters to indicate that they will not ban open-loop scrubbers. Some have even revoked bans following the publication of academic research into scrubber washwater.

A constantly changing playing field

With so many details to iron out on the route to IMO 2020 compliance, an increasing number of shipowners are turning to ship managers for guidance. While scrubbers offer a “shortcut” solution, LNG appears to be the most cost-effective option in the long term, providing there is sufficient infrastructure. LNG may even become more attractive as the market adjusts and the cost of very low sulfur oil falls. But as with many other regulatory matters in the maritime industry, including ballast water management, there is no one-size-fits-all solution. The considerations are many; the debates are endless.