In 2020 the Covid-19 pandemic wreaked havoc on just-in-time supply chains, and productivity at factories and distribution centres cratered across the world. The ramifications are still being felt, half a year later.

Unsurprisingly, during 2020 this was accompanied by a dearth of newbuilding activity, but the pandemic was far from the only reason for this. Regulatory uncertainty abounds, as the IMO targets a 70% emissions-reduction per vessel, but without a concrete notion of how to achieve it. This remained largely unchanged in the early months of this year.

But then, something extraordinary happened. Backlogs of cargoes in warehouses caused a worldwide container shortage; ULCV Ever Given blocked the Suez Canal for six days; a late outbreak of Covid in China caused port closures and queues of more than 40 vessels at a time; delayed repair works took many ships off the water; and long-term charter deals spanning four years or more became more common as wary charterers agreed to lock in rates in case the madness continued.

“The owners are really in the driving seat now and are looking to lock-in high daily hires for as long as possible… there is hardly anything coming onto the market, and what there is going to the highest bidders,” said an anonymous broker quoted in the Loadstar.

This unique combination of factors left customers desperate, and many started paying top-dollar for spot-market vessels – anything to get their goods to where they were needed in a reasonable timeframe.

In one example, American homeware retailer Home Depot said that its freight costs had risen so high that it has elected to cut out the middleman and contract its own container ship directly.

As a result, a handful of shipowners, with the right tonnage in the right markets at the right time, started making an absolute fortune. In June, S Santiago – an otherwise not particularly exceptional 15-year-old 5,060 TEU container ship – secured an astronomical rate of $135,000 per day for a 45-day round voyage, with an option on a second. According to FreightWaves, the vessel earned back one sixth of its total $38.48m value in a single voyage.

S Santiago was joined by 16-year-old 5,042 TEU CSL Santa Maria, with a similarly fantastical $160,000 per day for a three-month charter. Another smaller vessel, A Fuji, secured a six-month charter deal at $87,000 per day.

The common factor for these vessels? They are small enough, and old enough, that deploying them on the spot market, rather than long-term charter agreements makes for better economics. Particularly intriguing is the fact that construction of vessels in the sub-10,000 TEU size bracket has, according to data from Alphaliner, been nearly nonexistent since 2017.

Between June-July 2020 and the same period in 2021, container charter rates as a whole have increased from sub-$15,000 averages to $80,000.

This makes it more cost-effective for owners to buy vessels outright rather than charter them in, spurring an unprecedented ordering spree – or arms race, to some. Time is of the essence, and acquiring existing tonnage, rather than waiting for new ships to be built, is the ideal: in the secondhand panamax segment, sales are up 780%.

But newbuilding activity is staggering, too. Hapag-Lloyd is buying five 13,000 TEU newbuild resales, delivering between 2022 and 2024, and chartering another five on long-term agreements.

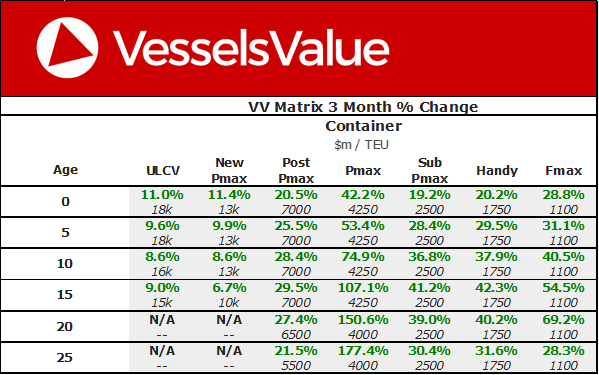

There is evidence to suggest that panamaxes are the most sought-after for the moment, with their valuations soaring, almost tripling in some cases, most likely brought on by the widening and deepening of canals, ship channels, and port berths coupled with the traditional economies-of-scale wisdom.

{kind=link}

Despite recent events having demonstrated a surge in demand for vessels in the sub-10,000 TEU categories, few expect a shift in container shipping’s philosophy for the foreseeable future. BIMCO chief shipping analyst Peter Sand told the Financial Times that “…ultra-large container ships are the preferred choice of ‘weapon’ in the arms race of the container shipping industry seeking to improve long-term profitability.”

Speculation as to the future outlook is mixed, with some calling the incident a “bubble” soon to burst – a tale familiar for industry veterans – and yet others indicating that the supply problems causing this boom in charter rates will not be alleviated for a while. Owners have rushed to buy panamaxes and post-panamaxes in response; but the success of vessels like S Santiago should show us that there is still room in the market for smaller ships.